")

As you know, the housing market has been robust over the last six months. Redfin just reported that home prices had increased another 15% as of October 23rd, and 56% of its homes for sale went through bidding wars.

Much of this has to do with lower supply and higher demand, coupled with extremely low-interest rates.

So what should you do if you are in the market to buy? Should you wait and see prices level and supply increase? Or should you commit as prices continue to increase?

While I can’t predict the future on what prices will do, I can provide some guidance on taking advantage of low-interest rates.

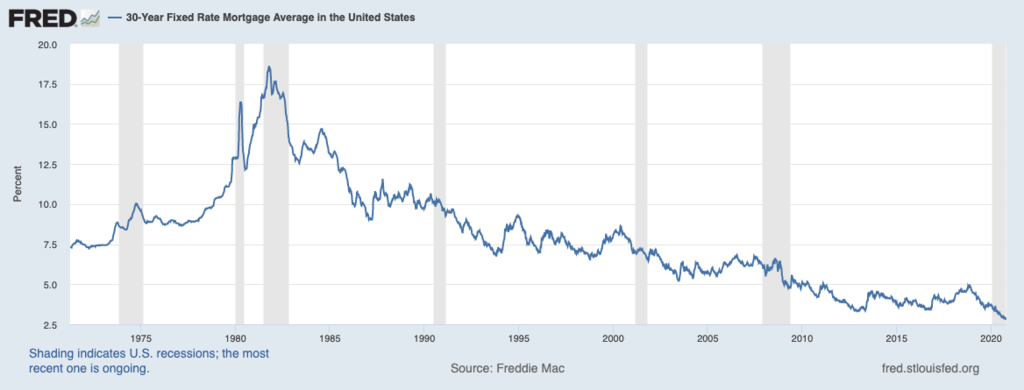

At 2.8% (October rates), interest rates are the lowest we have seen on record. Just take a look at the chart below from the St. Louis Fed.

Given the record lows in interest rates, if you are considering buying a home, your analysis should factor in the savings you gain on a 30-year mortgage rate compared to past levels or potentially higher future levels.

I will provide you with a quick comparison of how impactful low interest rates are in long term savings on mortgage interest.

Let’s compare two 30-year mortgage scenarios where everything is the same except for the interest rate.

In scenario one, the 30-year fixed interest rate is 3.8%, similar to what it was in October 2015 (5 years ago). In scenario two, the 30-year fixed interest rate is the October 2020 average of 2.8%.

Here are the inputs for a 30 year fixed mortgage comparison:

Median home price in Atlanta: $310,000

20% down payment: $62,000 (note that you can put as little as 5% down)

Interest paid after 30 years:

Scenario 1 at 3.8%: $168,185

Scenario 2 at 2.8%: $118, 850

Difference between scenario 1 & 2: $49,335

So while a 1% interest rate change may seem like a small number, it adds to massive savings. By taking advantage of low interest rates, in the above analysis, you could effectively save $50,000 on the lifetime cost of your home.

Interest rates could stay at this level for a while, or they could move. Again, I cannot predict the future economic environment.

However, I recommend considering that interest rates could change. Therefore, looking at the opportunity cost of taking advantage of the current low interest rates should be part of your home buying analysis, not just the home price.

If you interested in buying a home in Atlanta, let me help you do an analysis and find the right home for you. Contact me here.