As we get into the fall season, I continue to see strength in the residential real estate market. With recent rate cuts and the latest data analysis over the past three months, I believe we will continue the positive momentum from the summer into the fall.

In this post, I will provide an update on both the national and Atlanta residential real estate markets.

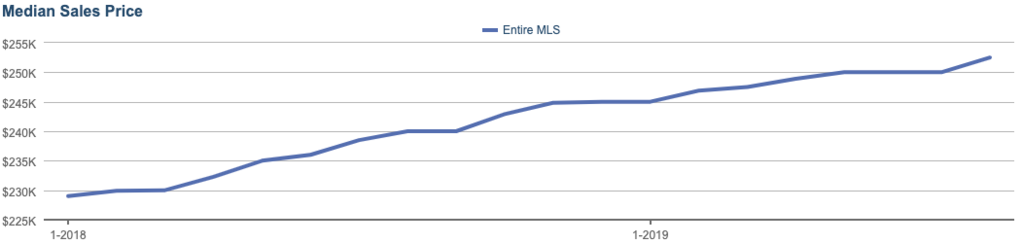

National Market

Median US home sale prices were up 5.2% in August, on a rolling 12-month basis. The median home price in May was $252,500. This growth is slower than the growth measured at the same time last year. Nevertheless, we continue to see steady growth in the US residential real estate market and an ongoing positive outlook for sellers.

The average number of days homes have been on the market in August increased by 7.5% from the same time last year. This trend could be helpful for fall buyers looking for a little more leverage. Comparing this to August 2018 there was a slight decline in average days on the market.

Likewise, In August, we’ve seen an uptick in supply of 10.7% over the rolling 12 month period. This is most likely influencing the increase in the average number of days on the market as buyers now have more choices.

All of this indicates that we continue to trend toward a more balanced market. In fact, new construction increased by 12% in August. This is a good sign that the market is still healthy, as builders see ongoing demand.

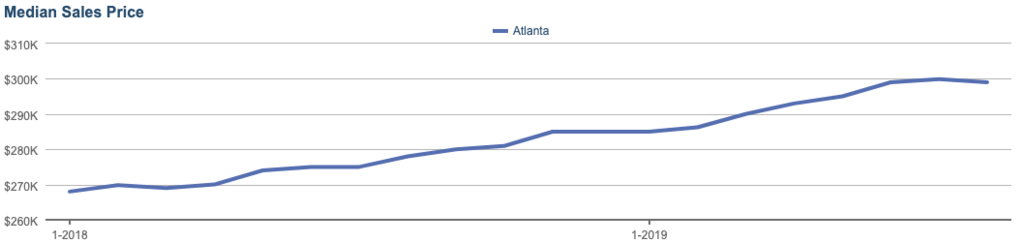

Atlanta Market

Atlanta continues to outpace national growth. Median Atlanta home sale prices were up 7.6% in August, on a rolling 12-month basis. The median home price in August was $299,000, well above the national median price. Comparatively, in August 2018, the median home price was $278,000.

The average number of days homes have been on the market in August increased 5% from the same time last year. This is lower than national averages, indicating that Atlanta still has strong competition and continues to lean towards a seller’s market.

Nevertheless, monthly supply continues to increase as more new construction projects are completed, which is favorable for buyers. Supply has increased by 30% since August of last year. Despite this significant increase, Atlanta is still struggling to meet demand and therefore has not seen a significant shift to a full buyers market yet.

With low-interest rates, strong price growth, and new construction becoming available, I expect Atlanta to maintain both a strong selling and buying market through the fall and winter months.

Are you interested in buying or selling your home this fall, taking advantage of the Atlanta growth new inventory? If so, please do not hesitate to contact me.